EXCLUSIVE: The Surprising Defense Sam Bankman-Fried Tells Me He’s Taking to Court

I met with Sam Bankman-Fried. He gave me his surprising defense.

By: Zack Guzman

August 2, 2023

Before Sam Bankman-Fried was placed under a gag order last week, I visited him at his parents’ house in Palo Alto to discuss the prospects of a possible interview.

I showed up to the home near Stanford’s campus on a Sunday and was immediately greeted by a security guard who informed me I’d have to leave all electronics with him outside. As was discussed in detail during recent court hearings, those are the conditions of SBF’s bail arrangement, along with having to record visitors on a pen register.

I had interviewed Sam before plenty of times, just never after being wanded down with a metal detector and certainly never while he was under house arrest. But this time I wasn’t just there to pitch an interview – I was there to pitch Sam on a new way of getting to the truth.

Three hours later, I’d leave with Sam agreeing to answer questions from the Coinage community – and something else I was never expecting to get: Pages of documents outlining his defense strategy and exactly what he says led to FTX’s downfall.

As a community-owned Web3 media outlet, Coinage will be breaking down everything we received together and curating still unanswered questions in our token-gated channels. (The chances of being able to deliver on an interview have now diminished a bit, given that prosecutors are pushing to revoke bail and detain Sam ahead of his trial. Nonetheless, as his defense team fights to maintain Sam’s ability to respond to press requests, we at Coinage want to be prepared. You can join in submitting questions here by minting a Coinage Caucus membership pass to co-own our outlet via our DAO/Cooperative.)

I realized after our meeting that Sam has been speaking with a number of journalists at various publications while under house arrest. A court hearing last week revealed Sam held more than 1,000 calls with members of the media, including more than 100 calls with a reporter at the New York Times. While the New York Times did not explicitly tell its readers how it received excerpts from Caroline Ellison’s private diaries, prosecutors learned from SBF’s defense that they came from SBF himself.

Our intent over the next few weeks is not to blindly publish Sam’s defense in his own words, nor is it to play a part in a larger “strategy” prosecutors say Sam is weaving. Our intent is to look critically at new facts with our community members and outside legal experts and to curate questions to be asked in a future interview, should it still be possible. Given that the actual trial is set to begin on October 2, we also hope to inform people of expected arguments to come.

Analyzing SBF's Defense

One of the main pillars of Sam’s defense is somewhat obvious in hindsight, given the decision to participate in the New York Times story that has now landed him back in court facing the threat of being detained. Those specific diary excerpts published by the Times paint a certain picture of Ellison’s own estimation of herself as being in over her head as the CEO of Alameda Research.

“Running Alameda doesn’t feel like something I’m that comparatively advantaged at or well suited to do,” she reportedly wrote.

At last week’s court hearing, lead attorney for the prosecution Danielle Sassoon lobbied the judge to detain SBF until the start of his trial on the grounds that leaking diary entries were a coordinated attempt to “corruptly influence witnesses and interfere with a fair trial through attempted public harassment and shaming.”

But Ellison is just one of the government’s key witnesses opting to plead guilty and cooperate in the case against SBF. There’s also Nishad Singh, former director of engineering at FTX, and Gary Wang, co-founder of FTX. Despite all of them pleading guilty to charges and cooperating in the case against him, Sam didn’t communicate any ill-will towards them for doing so. In a calm demeanor while also constantly shifting a fidget cube during the entirety of our conversation, Sam told me they are doing exactly what would be expected of people in their position.

What they knew and when, however, can be distinct from what Sam claims to have known leading up to FTX’s collapse. When exactly they informed him of certain issues between Alameda Research and the fund’s position on FTX’s trading platform will become paramount in SBF’s outlined defense.

However, as legal experts tell us, there are elements of the charges brought against SBF that have less to do with the end result of FTX’s collapse in November and more to do with how the company was initially set up and operated. Most of the charges Sam now faces stem from money laundering and fraud allegedly committed on lenders and customers stemming back years prior to FTX’s downfall. As FTX’s new CEO John Ray’s has outlined in multiple reports, some of the company’s earliest banking applications allegedly misrepresented the truth. Ray’s latest report also reiterates that Sam has essentially admitted as much in prior interviews.

“Especially in 2017, if you named your company like ‘We Do Cryptocurrency Bitcoin Arbitrage Multinational Stuff,’ no one’s going to give you a bank account,” Sam said in one June 2021 interview cited in the report. “[T]hey’re just going to be like . . . we’ve been warned about companies with this name. You know, you’re going to have to go through the enhanced [due diligence] process. And I don’t want to bother with that right now; it’s almost lunchtime. . . . But everyone wants to serve a research institute.”

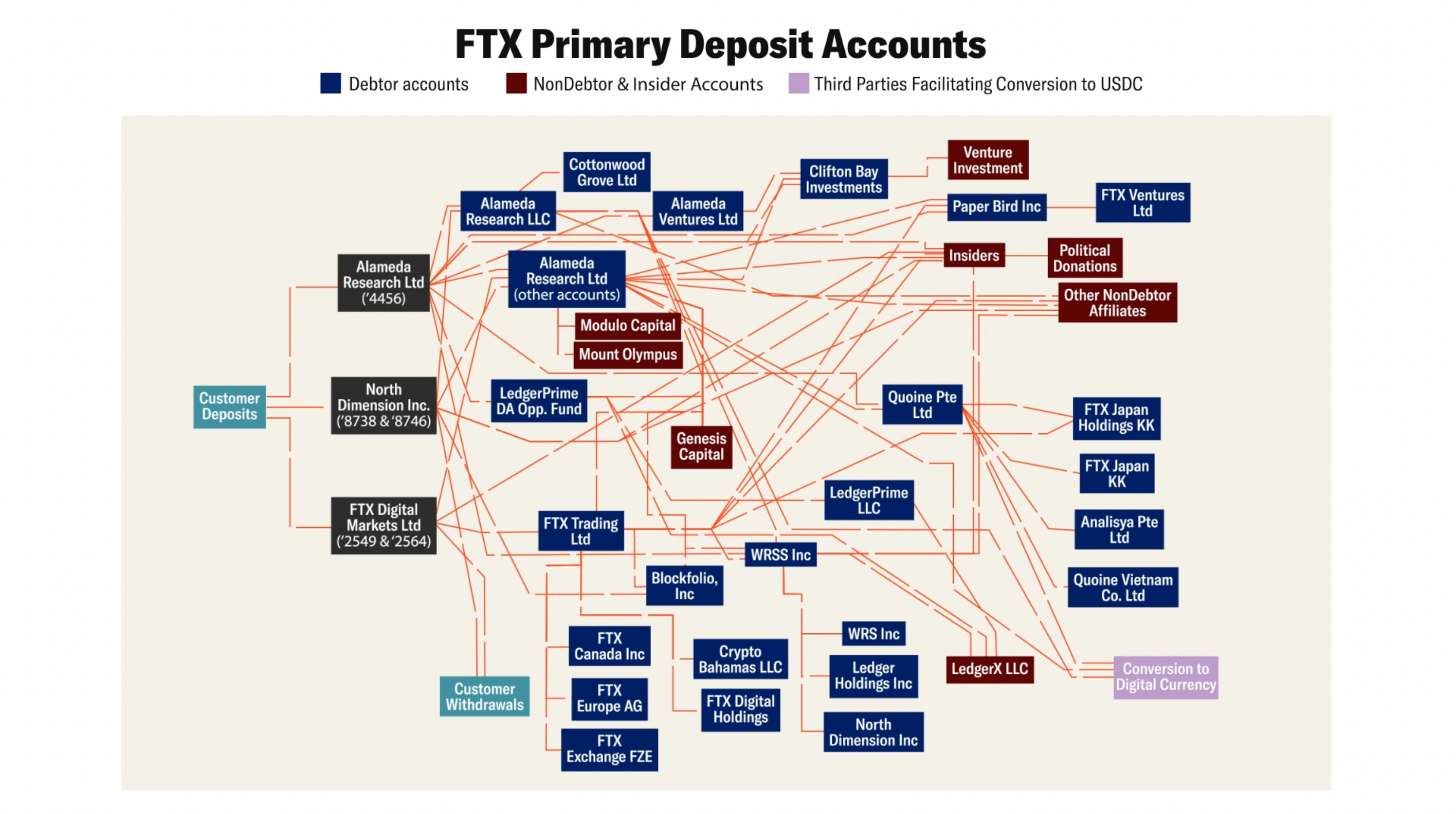

The banking complexity outlined in Ray’s latest report also highlights a tangled web of customer deposits flowing loosely without much distinction from Alameda’s accounts to others. As noted in a prior SEC lawsuit, FTX customers deposited funds into bank accounts controlled by Alameda due to FTX's trouble at securing its own banking relationships. However, the account tracking some of those balances, known internally as "fiat@," was poorly labeled, and the outstanding liabilities from Alameda to FTX were never settled properly, according to Sam, to the tune of billions of dollars.

In earlier interviews, Sam has cited the fact that he is not a coder as one reason he missed any account discrepancies. In furthering that point, his defense documents claim he was unaware of Alameda’s true liabilities until just weeks prior to FTX’s collapse. He also claims that neither Caroline Ellison, nor Gary Wang, nor Nishad Singh, nor other senior FTX developers who would have had the access to view the fiat@ account's balance told him early enough to address the issue before crypto prices unwound in November. Mismanaging trading risk was always a threat to Alameda. But without proper insight into Alameda’s exposure, Sam says he was unaware of the threat Alameda’s collapse could pose to FTX itself.

Beyond SBF's Defense

As we sat in his parents’ study, the ankle bracelet he was wearing started to beep. I realized a couple hours had passed since he started recounting some of what led to FTX’s demise, and we took a break from the timeline. It felt like the time to shift toward any personal reflections since his sprint of press interviews immediately after the collapse. After a swift swapping of batteries, Sam picked back up on something that had less to do with a legal defense as much as it seemed to do with a personal regret.

He’s tweeted about it before, but he tells me again that he’s still confused by the bankruptcy estate’s handling of FTX US. Notably – as he has documented on Substack – he reiterates his belief that FTX US should have never been included in FTX’s original bankruptcy filing, considering its financial status was separate from the crisis that brought down FTX International.

That seemed odd, given it was Sam himself who first tweeted about initiating the bankruptcy process for FTX while including FTX US and Alameda. But as he recounts, it wasn’t exactly a decision he reached without pressure from counsel at FTX’s formerly employed law firm Sullivan & Cromwell. Sam claims counsel with connections to Sullivan & Cromwell pressured him to file for Chapter 11 as the only remaining option, and later reneged on promises made to him before he handed over power of the company. After doing so, Sam says he was unable to select a new board chair as promised. Partners with the firm insisted John Ray be selected to steer the company though bankruptcy, according to Sam. After Ray was installed, he chose Sullivan & Cromwell as the primary counsel for the debtor entity.

A January affidavit filed by former FTX US Chief Compliance Officer Dan Freidberg highlights alleged conflicts of interest, given the pre-collapse relationship Sullivan & Cromwell had with FTX. Friedberg’s filing noted former Sullivan & Cromwell partner Ryne Miller lined up significant deal flow with the firm while working as general counsel at FTX US, including work tied to bailing out failed crypto lender Voyager Digital and filing various reports. A group of four U.S. senators, including Elizabeth Warren (D-Mass.) and Cynthia Lummis (R-Wyo.), also penned a letter echoing similar discomfort with the firm working on FTX’s bankruptcy noting “they may well bear a measure of responsibility for the damage wrecked on the company’s victims.”

“Any reputable law firm would withdraw from this matter and commence an internal investigation,” Friedberg wrote. “Instead, I expect [Sullivan & Cromwell] to take adverse action against me and disparage me publicly.” One day after John Ray published his second FTX interim bankruptcy report, FTX filed a lawsuit against Friedberg, seeking to recover damages allegedly caused by his breaches of fiduciary duties and legal malpractice.

In full disclosure, Sullivan & Cromwell is also, by extension, legal counsel for the estate overseeing Alameda Ventures’ investments, which includes an early 2022 investment in Coinage’s Web3 production company Trustless Media. Neither Sullivan & Cromwell nor FTX responded to Coinage’s request for comment. In a January court filing, the firm refuted that Sam was ever pressured in any leadership decisions, saying he consulted with his father and other lawyers before appointing John Ray, and that it was John Ray who filed for bankruptcy protections.

On Monday, the FTX debtor entity filed an updated reorganization plan that hinted at plans to reboot, with the possibility of relaunching an offshore exchange. Legal fees associated with FTX’s bankruptcy process have already surpassed a total of $200 million – more than double the legal costs incurred by crypto lending platform Celsius in its bankruptcy process over the same time period.

This week, Judge Kaplan is expected to rule on the government’s motion to revoke Sam Bankman-Fried’s bail and detain him before the trial begins. On Tuesday, Sam's attorneys filed a motion to defend his ability to address questions from the press and lift the imposed gag order. We will begin compiling questions now.

As we have with every major story, Coinage will continue to cover the trial proceedings and developments transparently with the help and guidance from our decentralized community. If you’d like to join in our pursuits to expose truth in crypto and control the larger crypto narrative, there has never been a better time to join our project.

READ INSIDE SBF'S DEFENSE, Part I, featuring the prosecutor who took down Bernie Madoff.

To support our community-owned outlet, own it with us, and unlock exclusive benefits, mint one of our Membership Passes today! Chat with Coinage in our Discord.

Disclosure: Alameda Ventures is one investor among many in Coinage's production company Trustless Media.