SBF’s Defense, Part 1: FTX’s Collapse Began With Caroline Ellison Taking Down Alameda

In order for Sam Bankman-Fried to win, Caroline Ellison must lose.

By: Zack Abrams, Edited by Zack Guzman

August 4, 2023

There are facts about Caroline Ellison that everyone can agree on.

For one, she didn’t do a great job running Alameda Research — the trading firm started by Sam Bankman-Fried and Gary Wang that operated as a market maker on FTX.

Under the stewardship of Caroline as co-CEO, and later, sole CEO, Alameda was allowed to operate without guardrails on FTX. It could borrow limitless capital from FTX’s users, according to Caroline, without posting any collateral, paying any interest, or risking automatic margin calls.

In entries from Caroline’s own diaries at the time, as reported by The New York Times, she privately doubted her own competency. “Running Alameda doesn’t feel like something I’m that comparatively advantaged at or well suited to do,” she reportedly confessed.

According to SBF’s own accounting, Caroline failed to manage Alameda’s risk, despite his warnings. SBF also claims that Caroline covered up the fact that FTX’s exposure to Alameda was greater than he could see — a weighty claim we’ll cover later. In SBF’s estimation, Caroline managed to endanger not just the one of SBF’s companies that she took over, but also the one that she didn’t.

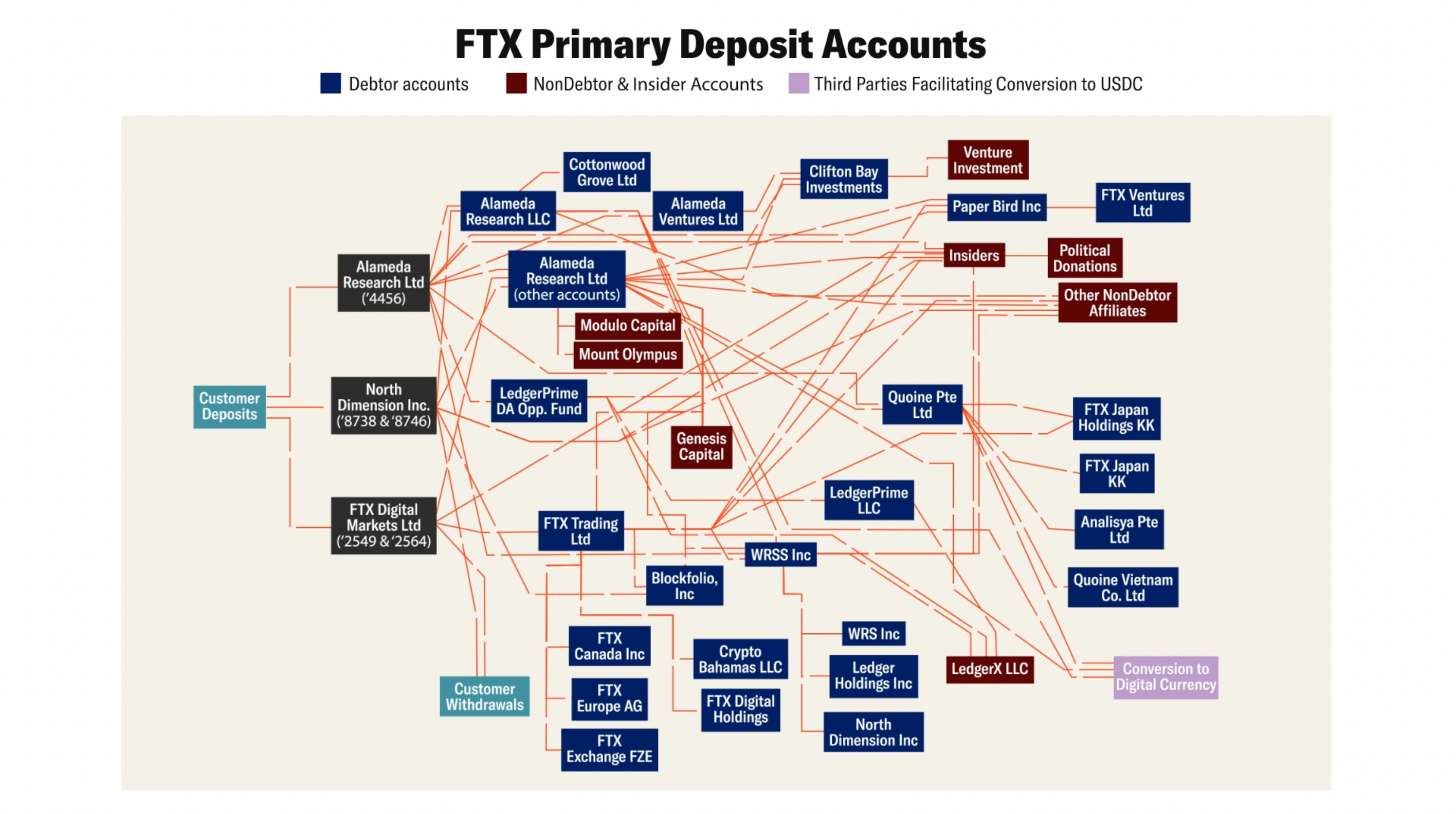

Another indisputable fact: Alameda and FTX were a mess. Attempt to trace the money moving through the ecosystem and you’ll end up with the spaghetti-like mess below.

The FTX empire ran on QuickBooks, and sometimes staff would approve expense requests with an emoji. A potential early investor in Alameda backed out because SBF could barely explain why the firm lost $10 million in a month. “We sometimes find $50m of assets lying around that we lost track of; such is life,” SBF once said.

The last indisputable fact everyone can agree on: Caroline Ellison is guilty. She pleaded guilty on December 18, 2022, to seven counts related to fraud and money laundering. In her statement to the court, she admitted to borrowing money from FTX in order to repay Alameda’s loans, working with SBF to retain Alameda’s lenders by giving them, “materially misleading financial statements,” and lending Alameda’s money directly to FTX’s executives, including SBF himself.

But SBF, as outlined in the defense he gave to Coinage before a court-imposed gag order, seems to be hoping everyone can agree on just one more point of order: Caroline’s guilt means Sam’s innocence.

For a reality check of the possibility that defense succeeds at trial, we asked former Bernie Madoff lead prosecutor Marc Litt. As he says, going up against three cooperators at trial isn’t necessarily impossible — it’s just unlikely. So how might SBF refute the three-on-one retelling of what happened from Ellison, his co-founder, and his head of engineering?

“One at a time,” Litt said.

EDITOR'S NOTE: As a community-owned Web3 media outlet, Coinage will be breaking down everything we received together and curating still unanswered questions in our token-gated channels. (The chances of delivering an interview have diminished a bit, given that prosecutors are pushing to revoke bail and detain Sam ahead of trial. Nonetheless, as his defense team fights to maintain Sam’s ability to respond to press requests, we at Coinage want to be prepared. You can submit your questions here by minting a Coinage Caucus membership pass, and you’ll also to co-own our outlet via our DAO/Cooperative.)

Alameda’s Meteoric Rise

SBF started Alameda Research in Berkeley, California in September 2017 with Tara Mac Aulay, who would quit the following April along with a “group of others…due to concerns over risk management and business ethics,” according to Mac Aulay. Despite this setback, Alameda found initial success exploiting crypto arbitrage trades in Japan; SBF claims that at the trade’s peak, Alameda was moving $25 million in Bitcoin every day.

Alameda’s peculiar name is no accident. In an interview from June 2021, SBF explained his reasoning. “Especially in 2017, if you named your company like, 'We Do Cryptocurrency Bitcoin Arbitrage Multinational Stuff,' no one’s going to give you a bank account. . . . [T]hey’re just going to be like . . . we’ve been warned about companies with this name. You know, you’re going to have to go through the enhanced [due diligence] process. And I don’t want to bother with that right now; it’s almost lunchtime. . . . But everyone wants to serve a research institute.”

In March 2018, SBF poached Caroline Ellison from Jane Street, widely regarded as one of the top quantitative trading firms in the world, to work for Alameda Research. A Stanford graduate, effective altruist, and Harry Potter enthusiast, Caroline would later tell Forbes it was “a really hard decision to leave.” Yet Alameda seemed like too good an opportunity to pass up; within a year of its inception, it was trading $600 million to $1 billion per day, according to a white paper from June 2019.

When SBF decided to start FTX in 2019, he quickly became absorbed with the operations of the nascent exchange. In the summer of 2021, he decided to resign as CEO of Alameda, appointing co-CEOs Caroline Ellison and Sam Trabucco to run the trading firm, in which he owned a 90% stake. Despite vacating the position, the CFTC claims SBF “...maintained direct decision-making authority over all of Alameda’s major trading, investment, and financial decisions” and regularly exchanged messages with Alameda’s staff.

The companies were officially separate entities, but in reality, FTX and Alameda were deeply intertwined. Early on in FTX’s history, Alameda was the primary liquidity provider of the exchange and its trades accounted for half of FTX’s total volume in the early days. However, according to SBF’s own accounting, Alameda made up only about 2% of volume on FTX by 2022.

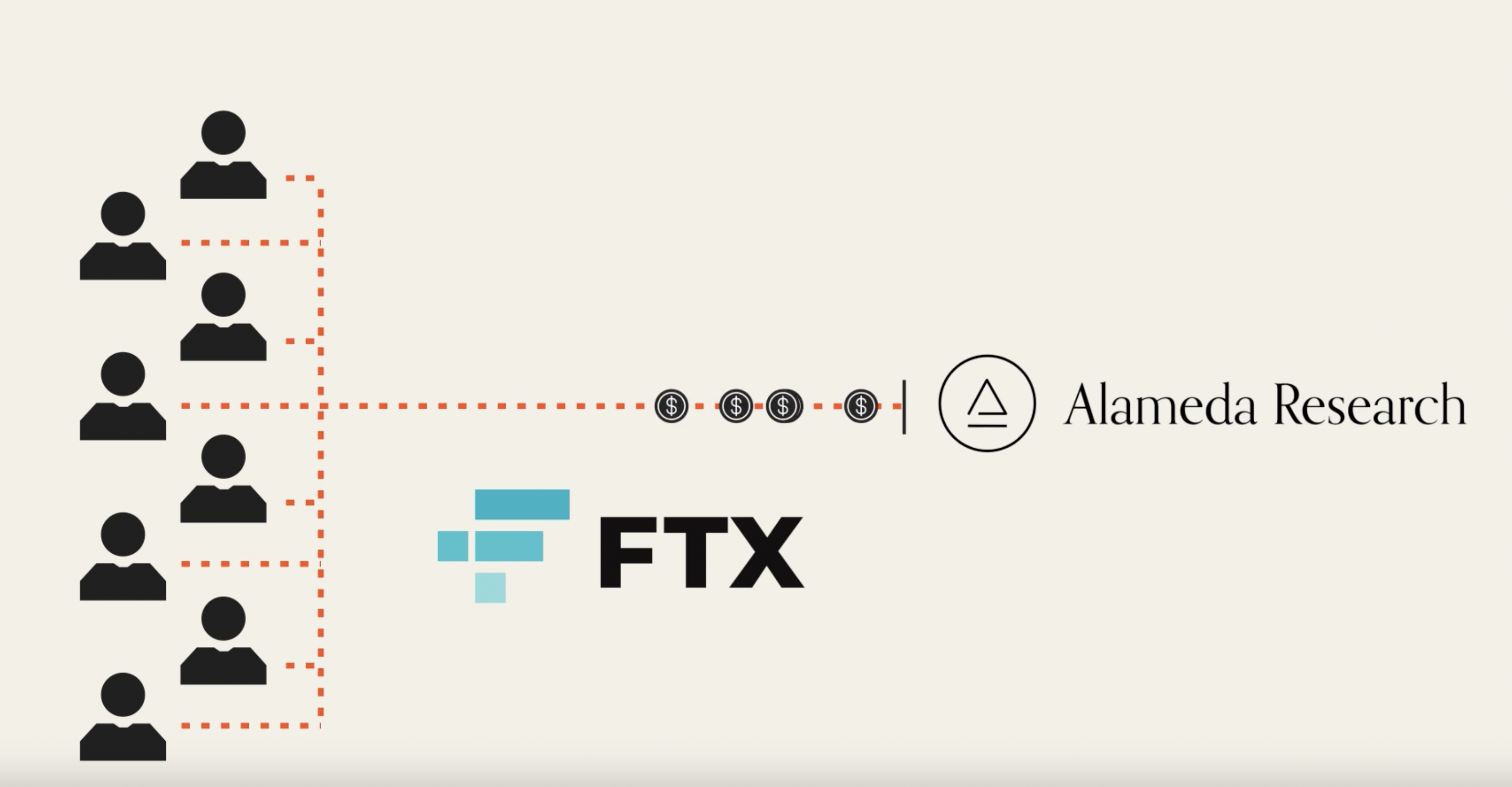

Alameda also acted as a payment processor for FTX through the end of 2021, according to SBF, accepting customer deposits on behalf of the exchange due to its trouble securing its own bank accounts. These deposits would eventually sum to $10 billion, and were located in an account known internally as “fiat@.”

Though SBF claims Alameda’s loans were fully collateralized, (the SEC’s complaint claims this collateral “consisted largely of illiquid, FTX-affiliated tokens, including FTT”) he admits that Alameda’s trading account was exempt from automatic margin calls, as liquidating the platform’s largest liquidity provider “would be chaos, and could be the result of a bug.” Instead, Alameda was given “a day or so” to add more collateral in the event it ran low.

SBF, in his re-telling, claims Alameda “had slower access to FTX than other market makers,” though the CFTC contests this in its complaint. SBF further claims Alameda “did not ever engage in predatory practices,” though the firm has faced allegations of trading with insider information from FTX.

As crypto prices began to skyrocket in early 2021, Alameda benefited both from its leveraged long positions and its venture capital investments in tokens like Solana and Serum. Alameda even borrowed as much as $13 billion in extra funds from third-party credit facilities like Genesis and Voyager in order to bet as big as possible, according to SBF.

Alameda’s bets paid off. By November 2021, Alameda, now with around thirty employees, had a Net Asset Value (NAV) of over $70 billion, according to SBF’s accounting. Yet just one year later, the trading firm would be effectively bankrupt, and its collapse would pose an existential risk to FTX.

Inside Alameda’s Collapse, According to SBF

SBF’s story of FTX’s collapse goes like this: A series of crashes in crypto prices cratered the value of Alameda’s assets. Caroline Ellison, having little risk management experience and feeling overwhelmed at her job, initially failed to hedge against the possibility of a crash, despite SBF’s suggestions that she do so.

By June 2022, according to SBF, Alameda had lost a fortune due to the downturn of the crypto market, its NAV crashing to about $14 billion. At that point, he threatened to fire Caroline, now the sole CEO of Alameda following Trabucco’s exit in early 2021, unless she hedged Alameda’s bets, and she complied.

However, in November 2022, customers rushed to withdraw billions of dollars worth of funds from FTX following fears of insolvency. This, in turn, caused the price of FTT to drop precipitously, making Alameda’s market hedges ineffective. In just a year, SBF calculated that Alameda’s NAV went from $75 billion to just $1 billion. Yet, there’s one more wrinkle to the story.

Remember the “fiat@” account, which reflected $10 billion of funds wired to Alameda but earmarked for FTX customers? According to SBF, those funds never made it to FTX’s bank accounts, likely because everyone had forgotten about it. There hadn't been any settlements of outstanding balances.

As the bank run on FTX continued, the extra $10 billion of Alameda’s liabilities threatened to push FTX underwater, or as SBF says, “Alameda's crash became FTX's liquidity crisis.” SBF takes care to point out that FTX was a profitable business, and one of the only firms in crypto projected to make as much in 2022’s bear market as it did in 2021’s bull. “In almost all senses, FTX wasn't the problem; Alameda was," he concludes.

SBF claims that he was unaware of the fiat@ account while it was in use. Since the account was only visible in FTX’s codebase and database, his lack of programming skills precluded him from seeing it. Furthermore, SBF claims Gary Wang and Nishad Singh, two of his deputies that pleaded guilty along with Caroline, “were aware of the general system, but were likely not aware of the details of fiat@,” while Caroline and the rest of Alameda’s staff were in theory aware of fiat@ but likely didn't pay any attention to it.

SBF claims he was first made aware of the fiat@ account in June 2022 after Caroline raised concerns that Alameda was nearing bankruptcy due to an unexplained $8 billion drop in assets over the first half of the year. However, FTX’s core developers soon found a bug in the account’s code and concluded that the shortfall was merely an accounting error. SBF, satisfied, set a goal to overhaul FTX’s accounting by the end of 2022.

It wasn’t until shortly before the November crisis, that SBF said he understood the full picture: While there was an accounting bug, after it was fixed, the fiat@ account still showed a balance of -$10 billion, meaning $10 billion had been wired to Alameda intended for FTX customers, but it wasn't properly accounted for on the FTX side.

SBF said that upon learning this, he demanded updated balance sheets for both Alameda and FTX in order to quantify the magnitude of the exposure. In his re-telling, he wondered openly why Caroline failed to mention that the company she was running, Alameda, owed $10 billion to SBF’s company, FTX — especially since, prior to fixing that bug, Alameda appeared to owe $18 billion to FTX. Perhaps she was embarrassed, he speculated, and insecure around him considering they had once been romantically involved.

That’s SBF’s story. But prosecutors are gearing up to tell a very different one.

“A Massive, Years-Long Fraud”

The story prosecutors will tell is similar to the one found in most media accounts so far: Sam Bankman-Fried and his inner circle, from the inception of FTX to its downfall, defrauded its investors, banking partners, and customers, along with Miami Heat fans, Tom Brady, and indeed, the whole world. As the SEC puts it in its complaint, “...Bankman-Fried was orchestrating a massive, years-long fraud, diverting billions of dollars of the trading platform’s customer funds for his own personal benefit and to help grow his crypto empire.”

SBF’s image as an effective altruist philanthropist lobbying for responsible regulation was an artifice meant to fool investors across the globe into contributing their capital, the complaint claims. While SBF touted FTX’s world-class risk management capabilities, Alameda was allowed to operate without constraint. And as FTX grew, the complaint alleges, SBF used funds from FTX users and spent lavishly on endorsement deals, advertising campaigns, political lobbying to both Democrats and Republicans, luxury Bahamian real estate for himself and his employees, and a variety of venture capital investments, including one in Coinage’s production company.

As his empire began to crumble, in part due to SBF’s willingness to let Alameda collateralize its loans using FTT tokens that were, the CFTC claims, “the same tokens whose market price Alameda’s trading desk was actively trying to control,” SBF continued, to the very end, to make false and misleading statements to investors in an attempt to salvage whatever remained. It only ended when SBF finally relinquished control and agreed to file for bankruptcy.

This fits neatly alongside the story Caroline Ellison told the world at her plea hearing. She admitted she was aware of Alameda’s special privileges on the exchange and the fact that Alameda was borrowing from FTX’s users in order to “lend” money to SBF and other FTX executives — money that was never expected to be repaid. She also admitted to misleading investors along with SBF by providing “materially misleading financial statements to Alameda's lenders,” and allowing SBF to make venture investments in Alameda’s name.

A cursory search will provide you with a whole host of other allegations of fraud, deceit, corruption, and recklessness. There are also some genuinely baffling ones. (Did he really consider turning an island nation into a doomsday bunker?)

“Such Is Life”

The story SBF gave us may or may not exactly match the defense he intends to present at trial. Much of it concerns the collapse of FTX and its aftermath, whereas several of his charges allege that the illegal conspiracies or actions began years earlier in 2019.

It’s also unclear whether or not SBF plans to testify. Marc Litt, the lead prosecutor on Bernie Madoff’s criminal case, tells Coinage that SBF may have to testify in order to establish he didn’t know about the fiat@ account. That would open himself up to cross-examination, which could open up a whole host of unsavory details, including the creation of all those bank accounts, such as North Dimension, a shell company (with not one but two sham websites) that was allegedly used to obscure ties to FTX.

“Maybe he will testify, but it probably won't go well, in part because he's done all of this talking since. So the prosecution has a lot, and they've got it all cued up and they'll be ready if he does testify,” Litt said. “Generally the cross-examination goes well for the government.”

And even if Caroline was truly responsible for Alameda’s demise, it may still appear to the jury that she was set up to fail. Caroline was appointed to her position (one she admits she wasn't comparatively advantaged at) by SBF, a romantic interest as well as a professional superior. The guardrails on Alameda’s accounts were removed. Regardless, Caroline has already pleaded guilty. So why hasn’t SBF?

In an internal communication, SBF once reportedly wrote:

“Alameda is unauditable. I don’t mean this in the sense of “a major accounting firm will have reservations about auditing it”; I mean this in the sense of “we are only able to ballpark what its balances are, let alone something like a comprehensive transaction history.” We sometimes find $50m of assets lying around that we lost track of; such is life.“

As SBF sees it, most of the counts he’s charged with are essentially restatements of the first count: wire fraud against customers. And he believes he’s innocent on that charge, because he never acted with intent to steal money from FTX customers using the fiat@ account.

Ultimately, it's likely the prosecution will tell this story: While Caroline Ellison may have played a part in FTX’s collapse, the FTX and Alameda empire was a house of cards built on one cardinal sin: Sam Bankman-Fried’s hubris.

Perhaps SBF thought that as long as Alameda had enough funds in the bank to cover any disaster that could conceivably befall his empire, it didn’t matter if proper procedures were followed. Bankers were obstacles to be avoided. Regulators were pawns to be manipulated. Or, perhaps, he was truly in the dark?

“I fully expect the defense will be: ‘It wasn't me, it was Ms. Ellison or whoever that was controlling it. But there's going to be more than one witness to say the opposite of that,” Litt told us. “And in my experience, the government wouldn't charge this as a, 'he said, she said,' case… there's Ms. Ellison, there are documents, and there's at least one other person, if not multiple other people, to corroborate what she's going to say.”

It will all be decided soon. But customers of FTX would be the first to remind everyone that it likely won’t change any part of the outcome for them. Sometimes there’s not another $50m of assets lying around. Such is life.

To support our community-owned outlet, own it with us, and unlock exclusive benefits, mint one of our Membership Passes today! Chat with Coinage in our Discord.

Disclosure: Alameda Ventures is one investor among many in Trustless Media, the production company behind Coinage.